10 Taboola Alternatives for Advertisers, Compared With Live Ad Data

Outbrain, MGID, Revcontent, MediaGo, the Microsoft Audience Network and five more Taboola alternatives, compared by what advertisers actually run on each network — not by sales-page claims.

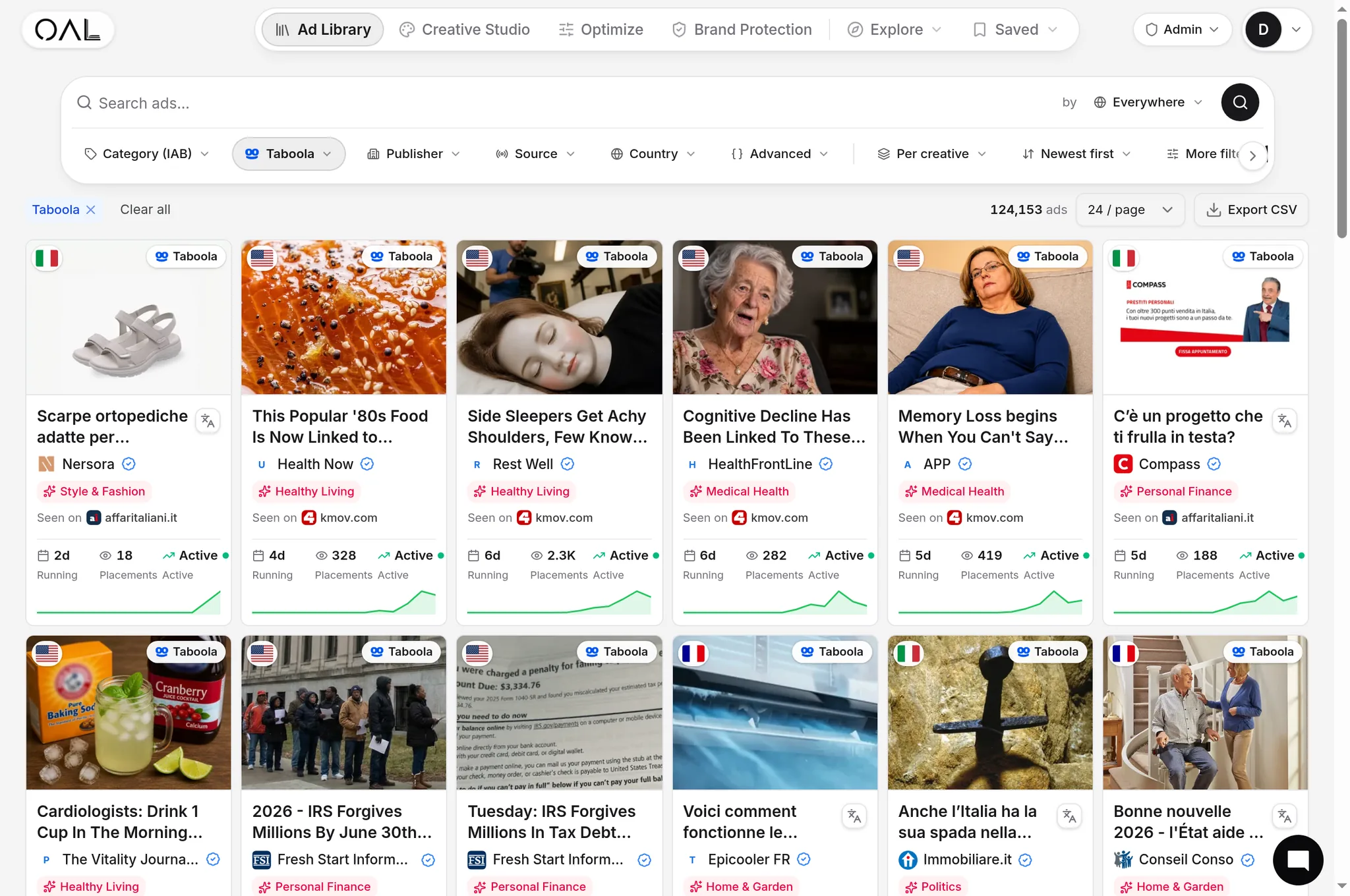

The strongest Taboola alternatives in 2026 are Outbrain (now part of Teads), MGID, Revcontent, MediaGo, and the Microsoft Audience Network — with Yahoo DSP, Teads' video arm, Google Demand Gen, Dianomi, and Nativo covering more specific use cases. Which one fits depends on three things: your vertical, your geo mix, and how much budget you can commit before a network's algorithm has enough conversion data to optimize. This comparison ranks all ten using live ad counts from OpenAdLibrary's index of 725,000+ native ad creatives across 49 networks (June 2026), so you can judge each network by what advertisers actually run on it rather than by its sales page.

Why advertisers look for Taboola alternatives#

Taboola is one half of the native advertising duopoly, and for plenty of campaigns it simply works — we broke down its mechanics in How Taboola Ads Work. But four pressures push buyers to diversify:

- Auction pressure in the money verticals. Health, finance, and insurance are Taboola's three largest verticals in our index — 11,982, 8,200, and 7,422 live classified creatives respectively (June 2026). Where advertiser density concentrates, CPCs climb, and the buyers feeling that first are the ones in exactly those verticals.

- Policy and review friction. Editorial standards tightened across the big native networks. Categories that clear review on one network can stall on another, and an account-level enforcement action on your only traffic source is an existential problem, not an inconvenience.

- Audience overlap. Taboola's feeds sit on many of the same premium publishers month after month. A creative that fatigues there hasn't fatigued everywhere — the same angle often gets a second life on a network with a different publisher footprint.

- Concentration risk. Any single-network dependency — one ad account, one rep, one policy team — is fragile. Media buyers who survived a Meta account ban already know this lesson; it applies to native, too.

Whether Taboola itself deserves your budget is a separate question — we looked at that in Is Taboola Worth It?. This article is about what to run alongside it, or instead of it.

How we compared these networks#

OpenAdLibrary continuously captures live native ad placements from public pages and network delivery endpoints, then stores the creative, the resolved advertiser, first-seen and last-seen dates, geo and device data, and the traced landing page. When we say a network has "X live creatives," that is a count of distinct ads observed running in our index as of June 2026 — evidence of real advertiser activity, not a press-release reach claim.

One honest caveat: index counts reflect our capture footprint, which is deeper on some networks than others. Treat them as relative activity signals, not absolute market shares. Networks where we don't yet publish counts are marked n/a below and assessed qualitatively.

The 10 Taboola alternatives at a glance#

| Network | Live creatives in index (June 2026) | Top observed verticals | Best for |

|---|---|---|---|

| Taboola (baseline) | 206,145 | Health, finance, insurance | Scale on premium feeds |

| Outbrain (Teads) | 108,573 | Insurance, finance, health | Closest like-for-like swap |

| MGID | 62,765 | Entertainment, health | Low minimums, Tier-2/3 geos |

| Revcontent | 15,789 | Health, finance, home & garden | Health and advertorial offers |

| MediaGo | 6,571 | Insurance, home & garden, ecommerce | Algorithmic buying on Microsoft supply |

| Microsoft Audience Network | 281,839 | Ecommerce, finance, travel | Untapped scale, search-adjacent data |

| Yahoo DSP (native) | 5,926 | Software, finance | Omnichannel programmatic teams |

| Teads (video-first arm) | 113 | Travel, ecommerce | Brand and video budgets |

| Google Demand Gen | n/a | — | Feed reach inside Google surfaces |

| Dianomi | n/a | — | Premium finance audiences |

Nativo, the tenth option, is a sponsored-content platform rather than a feed network — covered below with the specialists.

1. Outbrain (Teads): the closest like-for-like replacement#

Outbrain merged with Teads in February 2025, and the combined company now operates under the Teads name — but the feed product buyers know still runs, with 108,573 live creatives in our index (June 2026). Its vertical mix mirrors Taboola's money verticals almost exactly: insurance (4,345 classified live creatives), finance (3,990), and health (3,102) lead, which tells you the same direct-response economics work here.

The buying motion will feel familiar: CPC bidding, conversion objectives, feed placements on premium publisher sites. The publisher footprint overlaps Taboola's but is not identical, so a proven Taboola creative frequently finds fresh audience here. If you test only one alternative, test this one — and read our data-backed Taboola vs Outbrain comparison before splitting budget.

Watch out for: post-merger product renaming. Features move and dashboards get consolidated; verify current mechanics against official documentation rather than year-old tutorials.

2. MGID: low minimums and Tier-2/3 geo depth#

MGID carries 62,765 live creatives in our index, and its mix looks different from the premium duo: entertainment is its largest classified vertical (13,987 creatives), reflecting heavy content-arbitrage and celebrity-angle demand, with health second (1,220). Its publisher network runs long-tail and international — which is precisely its value. Media buyers scaling into Tier-2 and Tier-3 geos (LATAM, Eastern Europe, Southeast Asia) commonly report meaningfully lower CPCs than Tier-1 Taboola auctions, though your niche and geo move this a lot.

MGID pairs low minimum deposits with hands-on account managers, which makes it one of the cheapest ways to learn native buying. The trade-off is publisher quality variance: plan on aggressive placement blocking from week one. Mechanics, formats, and pricing are covered in How MGID Native Ads Work.

3. Revcontent: health and advertorial demand#

Revcontent is smaller — 15,789 live creatives in our index — but its demand profile is unusually concentrated: health leads (2,566 classified creatives), followed by finance (816), home & garden (789), insurance (638), and a meaningful nutra segment (440). That mix tells you exactly who makes this network pay: advertorial-funnel advertisers running health and wellness offers.

Reach is thinner than Taboola's, so treat Revcontent as a scaling channel for a proven funnel rather than a discovery channel for a new one. Creative review is stricter than the network's affiliate-era reputation suggests. Full walkthrough: How Revcontent Works.

4. MediaGo: Baidu's algorithmic buy on Microsoft supply#

MediaGo, Baidu's international native platform, shows 6,571 live creatives in our index, led by insurance (378), home & garden (301), ecommerce (265), and auto (257). Its pitch is machine-learned bidding — feed the pixel conversions and let the model find them — and its supply concentrates on MSN and partner feeds.

That makes MediaGo a genuinely different auction on inventory that overlaps the Microsoft Audience Network, sometimes at friendlier effective costs. It rewards advertisers with steady conversion volume and punishes thin-signal test budgets. Worth a slot on your test list if your offer already converts on feed traffic elsewhere.

5. Microsoft Audience Network: the biggest pool most buyers ignore#

Here is the number that surprises people: the Microsoft Audience Network is the single largest corpus in our entire index — 281,839 live creatives (June 2026), more than Taboola itself. The feed placements across MSN, Edge, and Outlook are bought through Microsoft Advertising, which means search-adjacent audience data, familiar campaign tooling, and easy expansion for anyone already running Bing search.

Top observed verticals are ecommerce (9,978), finance (9,029), travel (8,830), and insurance (8,406) — a broader, more mainstream mix than the affiliate-heavy mid-tier networks. The weakness is buyer tooling: it is a search platform's audience extension, not a purpose-built native DSP, so section-level control is coarser. Our MSN native ads guide covers the placement mechanics in depth.

6. Yahoo DSP: native inventory for programmatic teams#

Yahoo's self-serve native platform (Gemini) is gone; its native inventory — 5,926 live creatives in our index, led by software and finance — is now bought through the Yahoo DSP. That changes who it is for: DSP-level commitments put it beyond most small affiliate tests, but omnichannel teams get Yahoo's owned-and-operated properties (Yahoo Finance, Mail, Sports) plus programmatic reach in one seat. The history and the migration path are in How Yahoo Native Ads Work After Gemini.

7. Teads: the video-first branding arm#

Teads earns a separate entry from Outbrain because the buying motion is different even inside the merged company. Its heritage is outstream video and in-read placements on premium editorial, bought by brand and agency teams through Teads Ad Manager. Our native index tracks only its display-feed edge — 113 live creatives, led by travel advertisers like Flight Centre and education brands like Georgetown University — which itself signals the demand profile: brand budgets, not CPA arbitrage. If your goal is consideration rather than direct response, this is the branded end of the spectrum; see What Is Teads? for the full picture.

8. Google Demand Gen: feed reach inside Google surfaces#

Demand Gen is not a native network in the classic sense, but it competes for the same budgets: visually-led feed placements across Discover, YouTube, and Gmail. Strengths are Google's audience data and enormous reach; weaknesses are limited placement-level transparency and creative standards tuned for polished DTC assets rather than advertorial hooks. Buyers diversifying away from Meta often land here first, then discover that true native networks give them far more placement control.

9. Dianomi: premium finance native#

Dianomi is a specialist: native placements on financial and business publishers, serving fintech, investing, and B2B financial advertisers. Expect a qualified audience and compliance-aware ad review, with CPCs commonly reported above general-audience native networks — the premium is the point. If your offer is financial and your compliance team vetoes long-tail publisher feeds, this is the shortlist.

10. Nativo: sponsored content at brand scale#

Nativo places full sponsored articles — not just feed widgets — across premium publishers, keeping readers on the publisher's site. It suits brand and content teams with real editorial assets and consideration goals. Direct-response buyers will find the feedback loop slower than CPC feed networks; content marketers will find engaged reading time that widgets rarely deliver.

Which alternative fits your situation#

- Affiliate or lead-gen buyer on a tight test budget: start with MGID, then Revcontent if your vertical is health/nutra. Low minimums, forgiving economics, and you'll learn placement hygiene fast.

- DTC ecommerce brand: Microsoft Audience Network and Outbrain first — mainstream audiences and scale — with MediaGo as the algorithmic third test. Demand Gen if your creative is polished lifestyle imagery.

- Finance or insurance advertiser: Outbrain and Taboola remain the volume plays (their vertical data proves it); add Dianomi for the premium, compliance-clean layer.

- Brand and content teams: Teads and Nativo, in that order, with Demand Gen for reach.

- Programmatic teams consolidating seats: Yahoo DSP.

Before splitting budget, sanity-check costs against our native CPC benchmarks — and remember every network rewards a different creative temperature. What reads as a winner on MGID can fail review on Outbrain, and the ranking of the networks themselves shifts by vertical, which is why we maintain a live ranking of native ad networks by real ad volume.

How to sequence a multi-network rollout#

Adding a network is a test with one variable, and buyers who forget that end up with four half-funded accounts and no readable data. The sequencing that works:

- Port your proven funnel, not a new idea. The second network's job is to answer one question — does this network's audience convert on my validated offer? — so keep the offer, funnel, and creative angle constant and let the network be the only variable.

- Re-cut creative to spec, not to taste. Same angle, same story shape; adjust image crops and headline length to the new platform's requirements and re-check its content policies before submitting.

- Fund one network at a time. A meaningful test needs enough spend for a few hundred clicks per creative plus a learning period. Splitting that budget three ways buys you three inconclusive answers instead of one real one.

- Compare on cost per conversion after the learning period, not CPC on day two. Mid-tier networks often win the CPC comparison and lose the conversion-quality one; only the funnel math settles it.

- Keep the first network running. Diversification adds a channel; it shouldn't destabilize the one paying the bills while you test.

Most buyers land on a two-network core — typically Taboola plus Outbrain, or Taboola plus MGID for Tier-2-heavy offers — with a third account tested quarterly against whichever incumbent is weaker.

Vet any network before you fund the account#

The fastest way to waste a deposit is to test a network your vertical doesn't run on. Ten minutes of research prevents it:

- Look at what's live. Browse the network's actual inventory — OpenAdLibrary's Outbrain spy tool and MGID spy tool show live creatives, advertisers, and landing pages for free.

- Check your vertical's density. If you sell hearing aids and the network shows a deep bench of hearing-aid advertisers running 30+ days, the economics work there. If you find three ads, you're the experiment.

- Read longevity, not volume. Ads that keep running keep paying. A network where your competitors' creatives survive for weeks is a network worth funding.

- Trace the funnels. Landing pages tell you whether winners run advertorials, quizzes, or direct offers — which is your creative brief for that network.

Run the same check across every network in this list from a single index at /spy/native-ad-spy-tool, then fund the one or two accounts where the evidence is thickest. Diversification isn't running everywhere — it's running where your vertical already proves out, on more than one network.